We addressed the looming energy crisis in Europe in several articles, including the “War on Low Energy Prices,” It appears the day of reckoning is quickly approaching. However, they are choosing paths that I did not anticipate. In reaction to Russia closing the pipeline, the Europeans proposed two solutions; capping the amount that Russia would get paid for their energy or government-provided subsidies for their citizen’s utility bills.

The first of these is a non-starter. Oil and natural gas are both commodities which, by definition, mean they are indistinguishable from country to country. Rumors abound that China is already selling Russian oil to Europe at a premium despite the current boycott. Expect more of the same with a price cap where China can simply pay them a higher price and then re-sell “Chinese” oil to Europe.

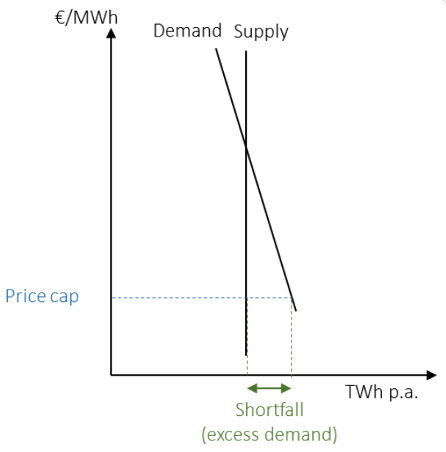

Subsidizing bills as a second choice hides the true cost of energy. This is clearly a horrible policy as it will support demand without increasing supply. This is illustrated nicely in the chart below, showing that this will create a gap where more people want power than is available. The likely result is rolling blackouts this winter.

A third choice is also being debated, which would make permits easier or cheaper to obtain. We discussed the Compliance Market setup at length previously. As a recap, emitters purchase a carbon allowance to balance their output with their measured pollution. Over time, the cost of these increase until carbon is eliminated or reduced to “safe levels.” Predictably, the current price for permits is surging as utilities scramble to produce energy in any way they can. This makes energy even more expensive than it would otherwise be, even with the government paying the bill.

With unsustainable energy costs, European governments left themselves little room to maneuver. The desire to focus on eliminating fossil fuels and nuclear energy appears to be ebbing. Perhaps this will save them. Headlines just this week reflect this change:

- UK to end fracking ban

- Germany to keep two nuclear plants open and burn coal

- France reactivating a closed pipeline to send gas to Germany

- Polish Prime Minster tells the Financial Times he would support scrapping ETS for a year or two.

We addressed the potential for a surge in bankruptcies due to the Covid “Bankruptcy Gap” just a couple of weeks ago in time for the August data to roll in. Sadly, it appears that the downward trend is shifting as all types of filing increased in August from this time last year.

This brings us to a driving force that will add additional stress. We predicted in May 2021 for our “Inflation Coming?” article that inflation might be inevitable, increasing the price of hard assets and commodities. This clearly occurred but seems to be moderating as the economy cools amid fears of a recession. As we described it, the Fed Pickle was that central banks could choose to keep on the rate path and risk economic contraction or back off for fear of a slowdown. They continue to push steadfastly to higher rates which are already affecting housing prices, reflected in the highest mortgage rates since 2008. While we may already be in a small one, the risk of a bigger “Recession Coming” is prevalent. Spiking energy prices in Europe and beyond, central banks raising rates while unwinding balance sheets, and geopolitical risks abound.

In an environment where choosing a theme for the economic story is difficult, I expect large positive and negative swings. Trading volumes should pick up as summer winds down as well. With policies changing by the day, we will continue to advise strategic allocations to alternative investments to keep portfolio risk in balance during the potential chaos still to come.

Photo by Pawel Czerwinski on Unsplash

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]