Archives

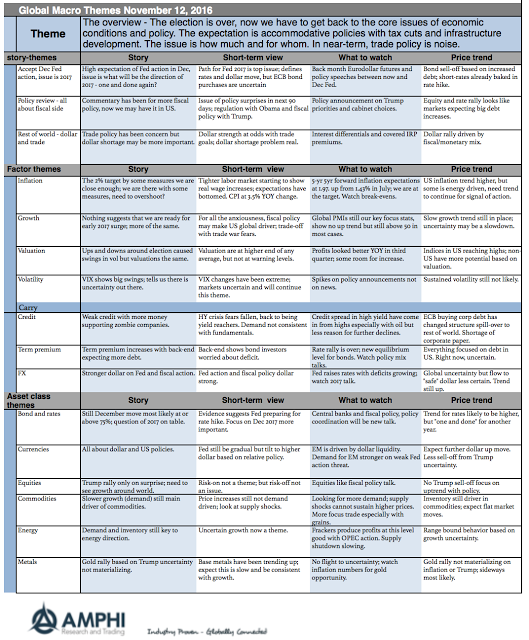

Global Themes on One Page

We have delayed our monthly global themes on one page given the US presidential election. There was too much uncertainty associated with the election to focus on the core themes of growth and valuation. Now that the election is over, we can focus on what is most important, growth, liquidity, and risk appetite. Financial markets are driven by the underlying economics of policies and not the personality of the president. Focus on policy, not the man. Personality matters to the degree that policy agendas can be moved. This is not trivial, but what moves markets are the policies. The key is determining what will get done, when, and how much. These policies have to be balanced with growth prospects around the world.

Liquidity Premium – Not Easy to Sort-Out

There is a strong demand for liquidity in all investments even hedge funds. However, there is a difference in the liquidity across hedge fund styles. The key investment question is whether you get paid to hold less liquidity. Is there an illiquidity premium?

Risk Hurdles

Risk management is more than applying quantitative tools to measure things like volatility or skew. It is an operational management problem of gathering and reporting data. The quality of risk management is related to the ability of a manager to properly aggregate data for analysis. Hence, strategies that have greater operational problems at gathering information on risk will have higher risk.

Hedge Funds

Hedge fund returns are a combination of alpha and beta risk exposure. The betas across different hedge fund styles are variable and dynamic. In general, beta will be below one, with most hedge funds showing market betas between .3 and .6. Some hedge fund styles, like managed futures, may be lower. Alpha can also be […]

Surprises Happen – Black Swan, No

Tail events will often lead to over-reaction as seen in the market action overnight. The worth of a manager is not measured by his ability to build and adjust portfolios in calm times but his ability to navigate and manage through uncertainty.

Navigating uncertainty is not always taking action but at times learning to do nothing. Discussion with managers suggests that some systematic managers did not take model signals last night. Markets moves out of proportion to the discounted futures cash flows signaled that no action was best.

Managing uncertainty starts with core portfolio construction. Extra diversification is necessary when there is extra risk. Diversification may come through differences in timeframe and styles when correlations across asset classes have the likelihood of moving to one. Managers are paid to build portfolios, manage risk, and take action on changes in economic fundamentals, this cannot generally be done with passive investing.

Sector Exposures

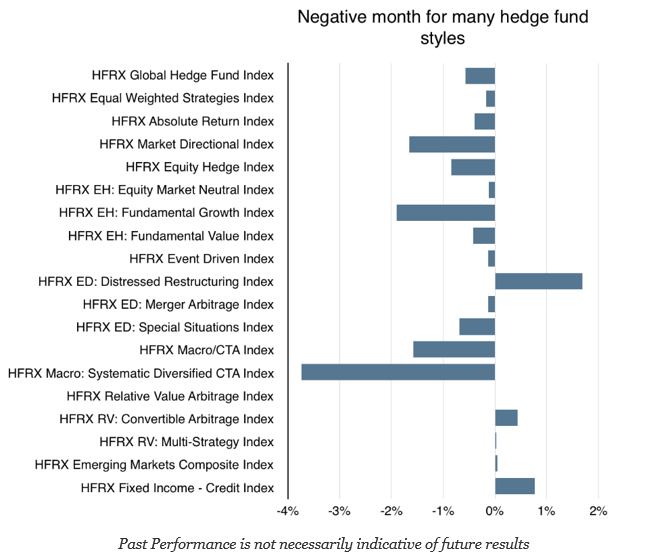

October was a painful month for investors with no place to hide in many sectors, styles, countries, or bonds. Major equity styles declined significantly especially in small caps.

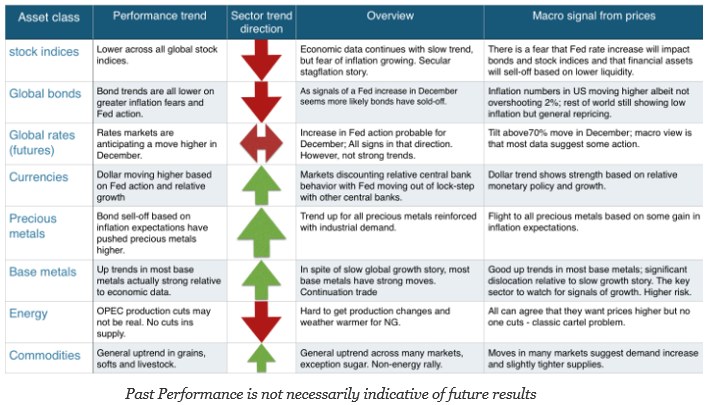

Current Trends

Each month we run a set of trend models against the major markets in each asset class sector. We then average the trend direction, either up or down, to generate a sector signal.

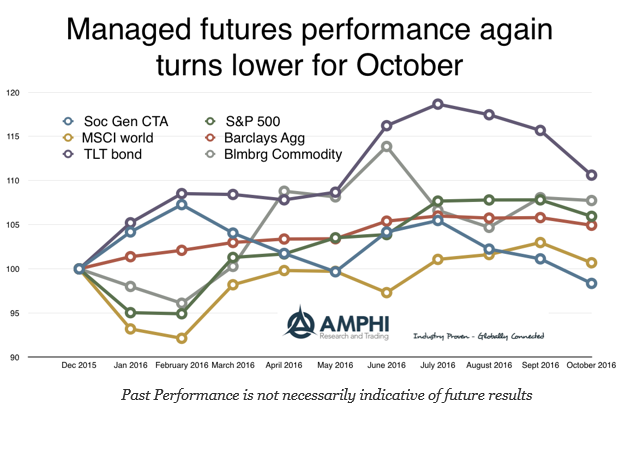

October 2016 Managed Futures Performance

Managed futures should not be synonymous with trend following but most of the major indices that track this hedge fund style have a high proportion of trend-followers.

3 Coping Strategies for Any Decision Process

The behavioral finance revolution has added immensely to our knowledge on the aberrations from efficient markets and rational expectations. Mistakes happen because we are sloppy thinkers.

Quantitative Analysis

A provocative post by Peter Lupoff the founder of Tiburon Capital called “When numbers cloud meaning – The fallacy of investment research exactitude” has me thinking about narrative versus the idea of false precision with quantitative analysis. First, something to put the issue into context; a classic joke on false precision, “I am 98.54% certain that you need both precision and narrative to be an effective trader.”

Crunch Time in Bond Markets Makes Equities More Vulnerable

Since the post Brexit plunge in bond yields, we have been becoming more negative on bonds. Along with virtually everyone, except central bankers, we have been banging the drum of how insane negative bond yields are. However, with many institutional investors required to hold Government bonds due to regulatory and capital requirements, and central bank’s QE exceeding global Government bond supply, it was almost understandable how bond yields could remain in sub-zero terrain. Understandable yes, but that did not make them good investments!

Cognitive Biases

The list of cognitive biases that can affect investors keeps growing. An explosion of studies show that observed decision-making under real and test conditions is hard. Just look at the wheel from Buster Bensen’s cognitive bias cheat sheet, the single best graphic I have seen which lists and categorizes the cognitive biases investors face, to get a flavor of the problem. Nevertheless, this work does a good job of reducing all of these biases into four problem categories:

Positive Skew

Skew can be an important component of returns. Obviously, investors would like to avoid negative skew, but if an asset with a positive skewed return distribution can be found, it can potentially generate a nice upside stretch with performance. Still, skew is sensitive to outliers and hard to measure. Skew is often generated from mixed distributions; nevertheless, if you can find positive skew investments and can associate this property with specific factors, portfolios can be structured to generate some extra upside return potential by increasing allocations to these assets.