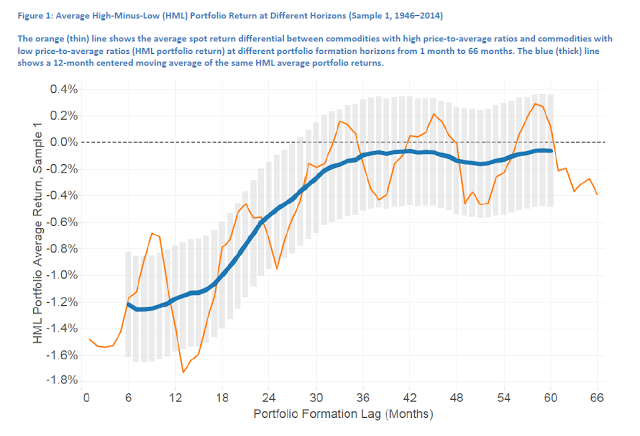

Momentum strategies work with commodity futures, but a closer examination shows that the same momentum strategies are ineffective with commodity spot prices. This result, that the cash price action is not mirrored in the futures prices, seems odd. Of course, the futures are expectational markets, but the cross-sectional behavior in the spot should be represented to a similar degree in futures. Alternatively, spot commodity prices show strong mean-reverting effects, while commodity futures do show this same behavior. These are the conclusions of research in the new paper, Momentum, and Mean-reversion in Commodity Spot and Futures Markets, by Chaves and Viswanathan. This research suggests that the momentum effect must be embedded in how the futures markets move relative to cash.

Several researchers have found momentum effects in commodity markets, so it would seem like a natural question to determine whether it is driven by behavior in the spot prices. The researchers find it is not, but they do find that spot prices are mean-reverting, which does seem consistent with the adage, “The solution to low prices is low prices.”

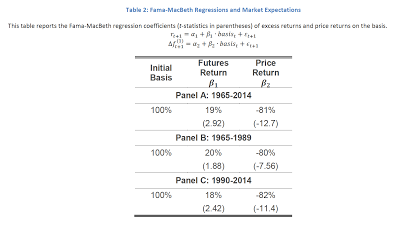

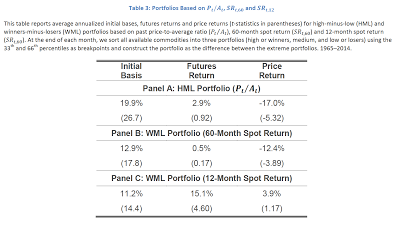

The only difference between the cash and futures prices is with the basis, which measures the link between the cash and futures, so this seems to be the natural place to look for why these differences between spot and futures exist. The researchers replicate earlier work by Fama-French to show that there is a risk premium in futures which could be an explanation for these results.

Using cross-sectional analysis, the researchers find that mean-reverting strategies do not work in futures because the futures seem to reflect the reversal in price. However, there are opportunities for momentum in futures prices when there is a significant positive basis.

The authors explain these interesting results, but I regard their work as preliminary. If anything, their work suggests a puzzle in the price dynamics of futures over spot. I believe that futures reflect storage and convenience yield in ways that are clearly not reflected in spot prices, but this will require more analysis to find the underlying relationships.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]