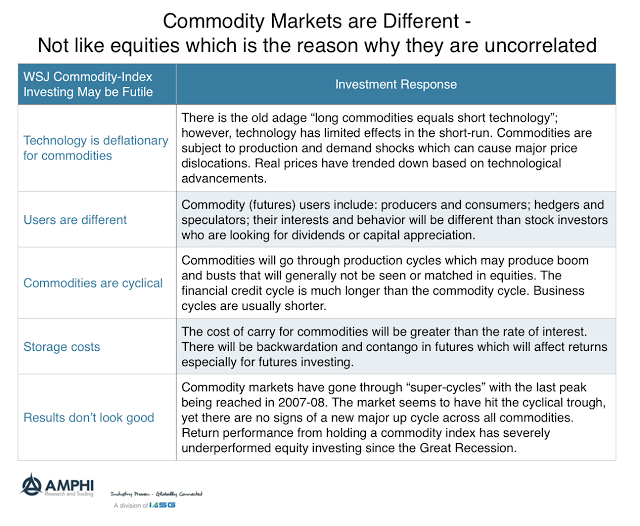

An article in the Wall Street Journal, “Why Commodity-Index Investing May be Futile,” has attracted much interest from investors. However, there was no new information in the story. The reasons for avoiding commodity indices should be taken seriously; nevertheless, the broader issue of differences between commodity and equity investing is straightforward. Commodity investing in an index of futures is not the same as a buy-and-hold strategy for an equity index. However, the factors that make it different are the reasons for the lower correlation of commodities with traditional investments.

Below are the five reasons why the WSJ thinks commodity index investing is futile and some elaboration on these differences. Simply put, different users and markets will lead to different return outcomes.

Is commodity index investing futile?

No, but a buy-and-hold strategy during market contango and low economic growth is a loser’s game. The idea that investors should just hold a long-term investment in a commodity index to get a range of commodity exposure has come and gone.

A few key issues must be answered to be a commodity index investor, even in the short run.

- Wheshort run a global business cycle? – Commodities peak late in the cycle, and there generally must be higher than expected growth to create excess commodity demand.

- Are there current supply shocks? – Along with strong demand, commodity investing needs to expect or have supply shortfalls for prices to rise.

- Are commodity inventories low? – For unexpected demand or supply shocks to significantly affect prices, commodity markets must be in a lower-than-normal inventory environment.

- Are commodity markets in backwardation? – The negative carry from market contango bleeds money for investors. Index investing needs backwardation conditions in futures which has not been the case for most of the post-Great Recession period.

- Is there higher inflation? – Many have discussed the relationship between commodity investing and inflation, but the link has been highly variable. Commodities have not been a reliable inflation hedge over the last ten years. Of course, this has also been a period of deflation or low inflation around the globe. Short-term dynamics and contango will dominate commodity index price moves in a 2% or less inflation world.

Commodity investing should be scenario-driven or situational and not buy and hold. Active management, where variable exposure is held in selected markets, may be a more reliable way of playing commodities. This can be done through sector exposure tilts to energy or agriculture or through active management of individual markets. This can be as simple as holding exposure in markets that show backwardation to some combination of momentum, carry, and fundamentals. However, active commodity management is still complex, so without solid conviction on the efficacy of active management, commodities should not be held as a core portfolio position.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

Gold’s Resurgence: Can Crypto Really Replace the Yellow Metal?

Once left for dead, gold speculators can sleep easily in 2025 as the yellow metal sits at all-time highs once again. Despite the shift to Bitcoin and other digital assets, the enduring nature of gold as an inflation hedge continues. What is driving this surge, and will cryptocurrencies still win the battle? Reasons for optimism […]