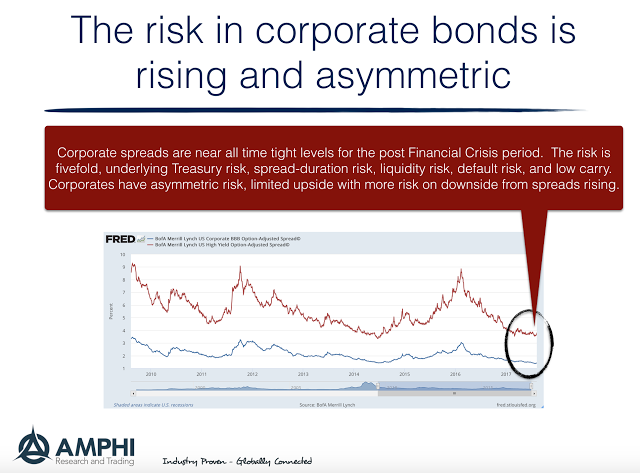

Corporate bond risk is rising. Of course, with improvement in the overall economy and continued bond flows many will not believe it, but the statistical data suggest that spread moves are no longer symmetrical. There is more potential for spread widening versus continued tightening.

For the post Financial Crisis period, BBB corporate spreads are now at some of the tightest levels on record and significantly tighter than average levels by over 100 bps. For high yield spreads the same story is also true with an even wider gap between current and average levels.

Default levels have fallen since the upheaval in the oil market so there would need to be further economic and company improvement to push spreads through all-time lows. There might be further tightening if there is a reduction in supply from corporations deleveraging, better earnings, or reductions of equity buy-backs programs. We have already see cuts in buybacks. On the other hand, it is possible that corporations believe there are better long-term investment prospects and there is actually an increase in borrowing to build new plant and equipment. Nevertheless, overhanging these macro drivers is the threat of a liquidity event if there is a reversal in buying.

The tight spread levels make choosing an alternative much easier. For example, the LQD ETF is currently at a spread of 150 bps over Treasuries with the same duration. This stand-alone hurdle rate for an alternative investment over Treasuries is significantly lower than a year ago. It is easier to make a switch and earn a comparable return.

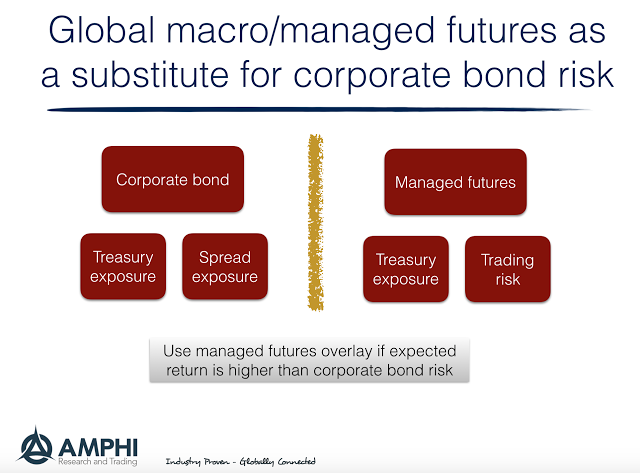

So what can be a good alternative to corporate bonds? We think it needs three things:

• A stand alone return of Treasury yields plus the corporate spreads.

• An uncorrelated return to corporate spread widening.

• A risk that is symmetric and not skewed to higher spread duration.

Managed futures or global macro could be a good alternative. First, managed futures could be done as an overlay on Treasury bonds as collateral through a separate account. This overlay will allow the trade to generate the Treasury returns and the excess return hurdle will be the spread on corporates. In this case, the managed futures investment has to generate at least a 1.5% rate of return to match the yield spread on corporates. While many funds are currently in a drawdown, there are also many managers that have generated high single digit annualized returns over the last three years with a symmetric risk profile. These managed futures returns should be uncorrelated with corporate spreads. An additional benefit is that if there is a dislocation or divergent event that will drive corporate spreads wider, it is likely that this will be good for long/short managed futures managers who generally do better when there is a market dislocation.

Switching to managed futures from corporate bonds achieves three goals: 1. a reduction of credit risk; 2. a switch into a strategy that may have more upside potential; and 3. an increase in the diversity within the overall portfolio.

DISCLAIMER:

While an investment in managed futures can help enhance returns and reduce risk, it can also do just the opposite and in fact result in further losses in a portfolio. In addition, studies conducted of managed futures as a whole may not be indicative of the performance of any individual CTA. The results of studies conducted in the past may not be indicative of current time periods. Managed futures indices such as the Barclay CTA Index do not represent the entire universe of all CTAs. Individuals cannot invest in the index itself. Actual rates of return may be significantly different and more volatile than those of the index.

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]