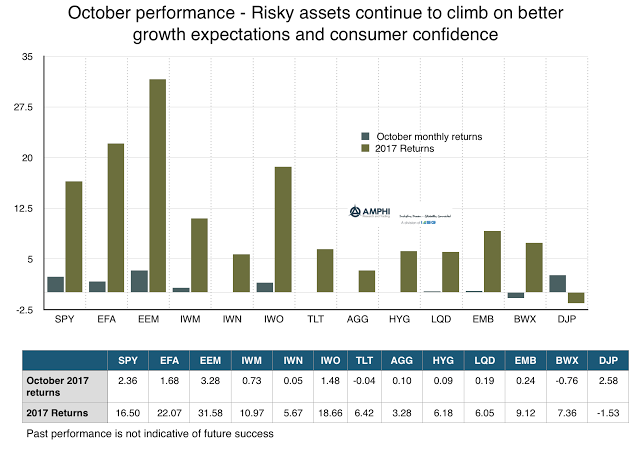

Talk of tax cuts floating through the halls of Congress coupled with stronger consumer confidence allowed risky assets to continue marching higher. Warnings of overvalued equities, concerns over leverage, and higher geopolitical risks, have not stopped stocks from stronger gains around the globe. For US companies in the third quarter, 76% have shown positive earnings surprises and 67% have had positive sales surprises. The earnings growth rate is 4.7% for the third quarter according to Factset. Positive economics, good company performance, and low volatility all contributed to this continued rally.

Bonds were generally flat with some positive performance in the credit area and a decline in international bonds after accounting for dollar returns. With further dovish behavior from the ECB and a Fed that is cautious about quickening any pace for rate rates, there is still good liquidity in the markets. Inflation is still below 2% as measured by the PCE even though other selected measures show stronger numbers. Controlled inflation has limited any bond sell-off.

The message from October is the same one we have been hearing for most of the year. Beta investing is in style. There has been little reason to look for diversification or localized opportunities. Investors are being paid to follow market direction and not focus on manager skill to control risk. This will change and the reversal may be swift, but right now there is no clear catalyst for a market reversal.