The take-away quote from Yellen this week, “The relationship between the business cycle and the yield curve may have changed.” There was little supporting evidence for her view. It is the hope of the Fed that further rate increases which may further flatten the yield curve will not reverse the current course of the economy.

The curve has not inverted, which is the actual sign of a potential recession, but has only flattened, albeit the flattening has occurred at a fast and more consistent rate in the last year. Bonds still do not have a risk premium, expected inflation has not appreciably changed over the last year, and higher growth has not moved the real rate of interest higher. Long bonds are not following the script of moving higher with the Fed normalization.

A link between a flattening yield curve and recession may be just correlation and not causation, but there are good stories for why there is a link. First, a flattening yield curve reduces the profit potential for banks. Banks may be less important with financing, but the shape of the curve does matter for their profitability and lending behavior. Second, a flattening yield curve changes the risk profile for moving out on the yield curve. There is less term premium for holding duration. Investors will less likely hold risker assets when you can be compensated with a high cash yield.

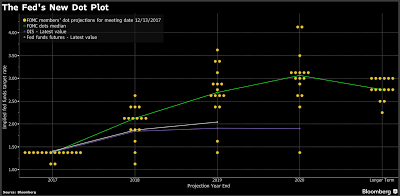

The meaning of the flattening of the US yield curve in the context of the Fed forward guidance is important. The Fed dot plot suggests that there will be three rate increases in 2018, another two or more in 2019, and likely more in 2020. Bonds yields suggest that traders do not believe the plots. The Fed has creditability with their longer-term forecasts.

Additionally, bond traders still have in the back of their minds the view that an overvalued stock market will need Fed support sooner than later. Another reason to put less stock in three Fed increases for 2018. In a global context, a tightening Fed coupled with continued savings around the world suggests that dollar denominated bond demand is still high.

There are a couple of implications for global macro and managed futures players. First, the big down trend in bond prices is not upon us. Strong trend signals are still not apparent and bonds may not be a place for greater profits at this time. Second, the further resolve of the Fed suggests that opportunities in the rate markets are increasing. Trading short rates has been relatively dormant for year, but Fed trends have led to price trend opportunities. Third, the continued rate increases provide a nice tailwind for returns on cash. Cash rates are now covering management fees for many funds. There will be fixed income opportunities but more will be in the front-end of the curve.