The origin of the word credit, credere, is Latin for believe or trust. So there is a simple question for any credit investor, do you believe that current outstanding credits can be trusted to payback all interest and principal over the next few years? It is a simple question and many who trusted payments a year ago do not have the same trust today.

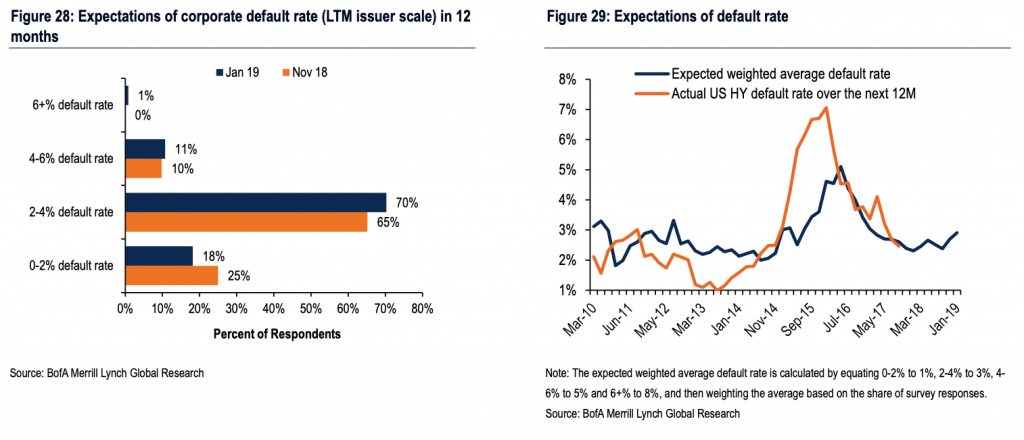

Default rates expectations are higher from BAML survey. Although not as high as 2016 levels, the default expectations are trending higher.

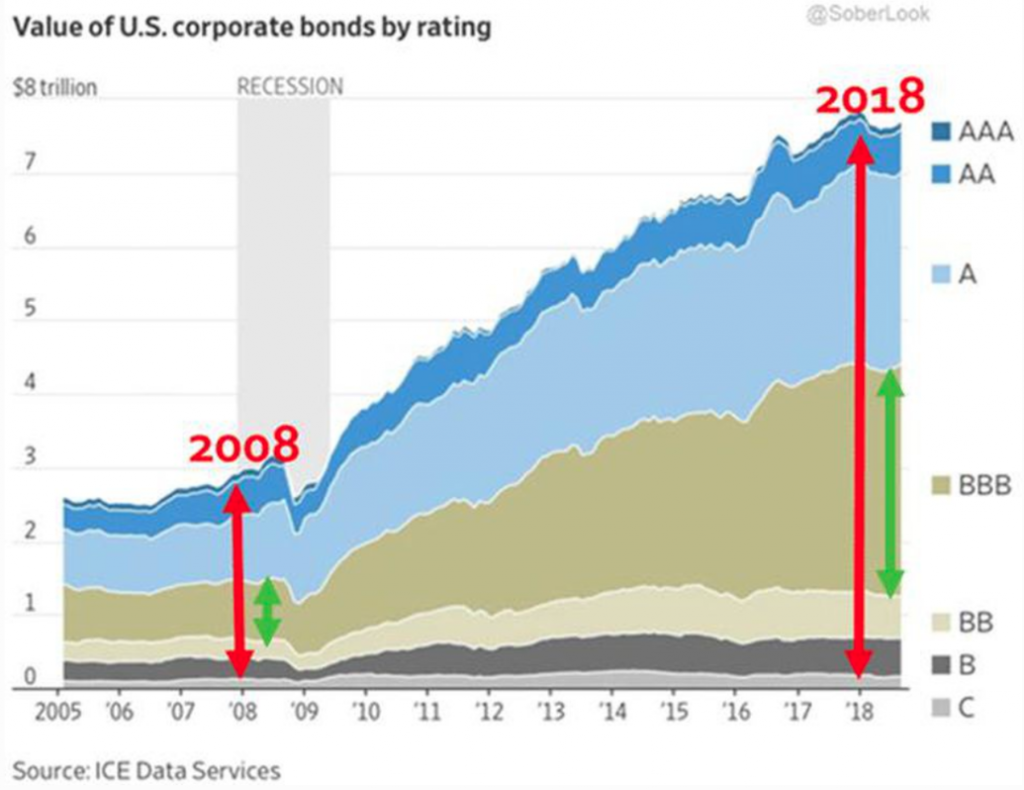

This is important because the size of risky debt is higher than ten years ago, and the growth has been especially high for BBB-rated firms.

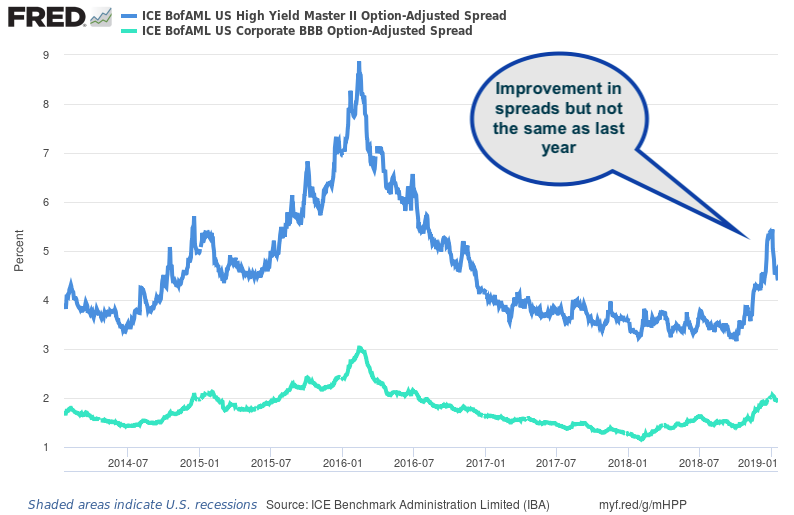

Spreads have widened both for high yield and investment grade although there has been reversal with the gains in equities this month. Certainly, volatility for spreads is at the highest levels in years.

Our view is very simple. Credit spreads are a risk premia attached to a Treasury bond. There is growing downside with being long this risk premia; consequently, it makes sense to diversify into other risk premia that have less downside.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.