Corporate spreads are tight and there is little room for further reduction given the absolute level of spreads. The reach for yield may be at an extreme. The bond spread is the compensation given bondholders for taking on the risk of corporate debt; consequently, it should become a concern when the quality of bond covenants or protections declines with spreads. Of course, if risk is declining, this is not the case, but at this point in the credit cycle it is hard to make that argument. An inverse relationship between spreads and covenant weakness means you are getting less compensation and less protection for the same risk, all things equal.

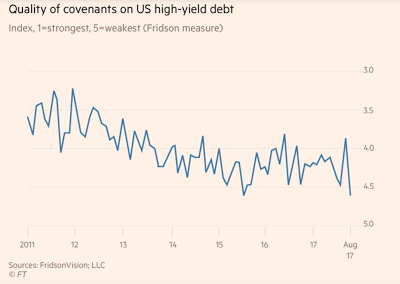

The Moody’s Covenant Quality score was developed to measure the change in bond structuring terms that will be detrimental to bond investor. It moves between 1 and 5 with 5 being the weakest covenant quality. It is now at all time lows.

There may be reasons for corporate debt risk to fall. Rates are low, so refinancing is cheap. Demand for credit is still high and debt to equity levels are manageable for many sectors. However, forward expectations suggest that return versus risk is less attractive from a structural perspective as bond covenants are loosened. Hence, opportunities should be found elsewhere.

An alternative is to exit the credit markets and hold liquid portfolio of dynamic beta bets through global macro and managed futures. Generally, managed futures traders do not take credit risk, so the return profile will be based on other risk premium such as momentum. A swap from tight risk premiums to those that may be less cycle dependent can improve the risk exposure of a portfolio.