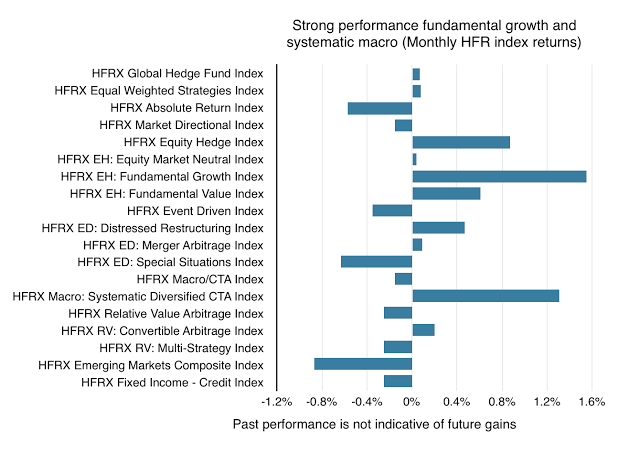

Hedge funds returns were mixed for November, but the fundamental growth and systematic macro strategies generated strong returns of over 1 percent. The fundamental growth strategy is the HFR leader for the year with a return profile at over 17%. The macro systematic strategy again generated a strong positive return. The HFR macro systematic index return was significantly higher than other systematic indices for November which suggest a high dispersion across managers in this category. The macro/ CTA which includes discretionary managers was actually down for the month. The absolute return, special situations, and emerging markets strategies were the biggest down strategies for the month, but all showed declines of less than one percent.

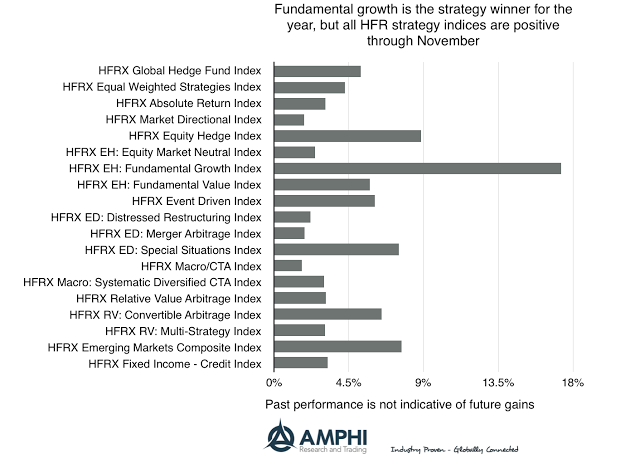

Hedge fund strategy returns are all positive for the year through November albeit the majority of the indices have returns below four percent. The outliers were strategies that have strong directional equity exposure. A fuller analysis relative to benchmark factors is needed to determine the quality of returns, but at this point even the diversifying strategies have outperformed traditional fixed income benchmarks.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.