Should investors be worried about credit spread return expectations or expectations of credit default losses in the current environment? Before we answer the credit questions about the current environment, investors may need a framework for weighting the types of risks in the credit markets. This is the fundamental question concerning holding any credit exposure, and an exhaustive research using variance decomposition of a large dataset shows that you should be worried about both. See “What Drives the Cross‐Section of Credit Spreads?: A Variance Decomposition Approach”, by Yoshiio Nozawa in the October 2017 Journal of Finance.

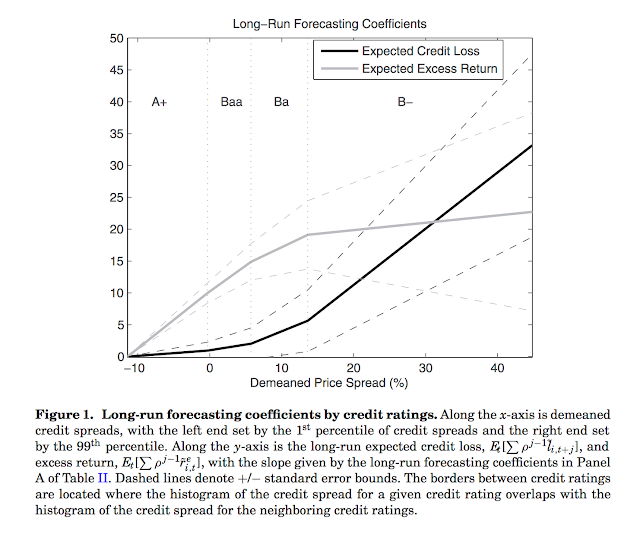

This work which follows a similar approach used to analyze variance decomposition on stocks shows that risk can be decomposed into an expectations comment and a default component. At the portfolio level the credit default risk is diversified away and the majority of risk is with changing expectations of risk premium. There are, however, differences in the weighting based on the credit ratings – the importance of credit loss is inversely rated to the credit rating.

The author focuses on the dynamic between stocks and bonds and finds that there is a distressed effect whereby firms with higher risk bonds closer to default actually have lower equity returns. There is a significant inverse relationship between credit loss risk and profitability but there is no relationship between bond and stock risk premiums.

This work is important when applied to current events. Credit default risk can be diversified away and time varying risk premiums can be the key driver of spreads which means that macro effects will likely drive credit spreads. Credit allocation decisions at the portfolio level are still a macro bet which may be closely tied to business cycle analysis. Spreads may move higher even if there are limited signs of greater credit defaults. Investors may face spread risk even if default rates are low.