DISCLAIMER:

While an investment in managed futures can help enhance returns and reduce risk, it can also do just the opposite and in fact result in further losses in a portfolio. In addition, studies conducted of managed futures as a whole may not be indicative of the performance of any individual CTA. The results of studies conducted in the past may not be indicative of current time periods. Managed futures indices such as the Barclay CTA Index do not represent the entire universe of all CTAs. Individuals cannot invest in the index itself. Actual rates of return may be significantly different and more volatile than those of the index.

Commodities have been an out of favor asset class. With a long-term return downturn, that has only partially reversed, many have avoided commodities even though it has been one of the best performing asset classes for 2016. A return of over 5% through November 11th as measure day the DJP total return has made it a strong gainer albeit the reversal in oil has caused declines from highs earlier in the year.

Avoidance of commodities seems natural given the 1, 3, 5, and 10-year annualized returns have been negative. No allocator who looks over past performance will touch this asset class, yet for those starting to worry about inflation and those who want better diversification, now is a good time to consider commodities. The current reasons for increasing commodity exposure were put together by Schroders in Reappraising the Case for Commodities. To summarize the current rationale for commodity exposure, we can focus on two issues. One, the threat for inflation is increasing and two, the need for diversification is also increasing.

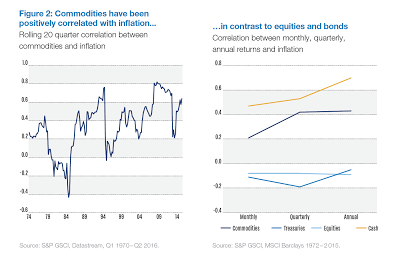

The correlation between inflation and commodities is the strongest for any asset class except for cash. This positive correlations occurs on a monthly, quarterly, and annual basis. If there is an expectation that inflation will be rising, then an increased commodity exposure makes sense. We have seen 5-yr/5-yr forward inflation expectations come close to 2%. The yoy CPI change is well above 2% and all measures of US inflation are off the lows. Granted global growth and inflation expectations have not increased, but positive inflation beta may be helpful in 2017.

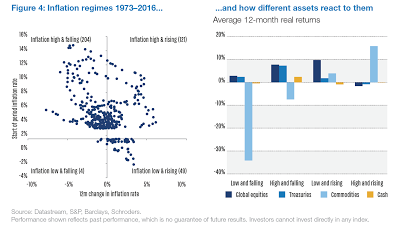

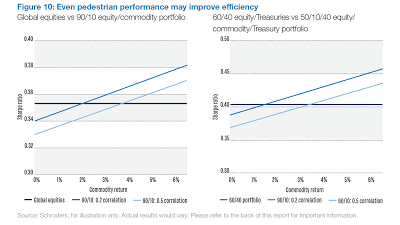

The inflation regime breakdown suggests commodity assets will do better than other asset classes except for global equity if we are in a low and rising rate environment. We think the combination of increases in global equities and commodities is a nice direction to take asset allocations.

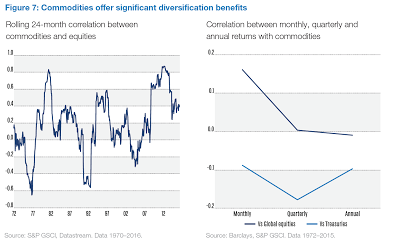

As important as inflation sensitivity for investors, is an increase in portfolio diversification. Given the talk of a bond bubble and the relatively high values for equities, any diversification would be helpful at spreading risks. The story that we find most compelling is the fact that adding commodities will diversify risks, but even a small positive increase in commodity returns will improve information ratios. We appreciate the current risks in both fixed income and equities, so any gain in commodities tied with the diversification will be a strong positive for investors.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]