Markets have been known to move to price extreme which have often been referred to as bubbles. The best known of these bubbles have been noted to lead to large market dislocations in both financial markets and the real economy. The “dot com” and housing bubble are the best known most recent examples, but unfortunately, there has not been much agreement on what are identifiable characteristics or the cause of these bubbles. While there can be agreement that bubbles are related to positive feedback loops, there is little work on a method for filtering data through some general model that will define a bubble.

The Financial Crisis Observatory (FCO) at ETH Zurich, formed by Didier Sornette, has developed models for identifying bubbles in financial market indices, sectors, and stocks through what it calls the FCO Cockpit. Given a well-established model based on price with explicit probability measures for a market reversal, the FCO can identify financial markets that are likely in a bubble state by looking at price behavior.

In reality, there are bubbles all over the world in many markets. There have been significant positive bubbles with large market increase as well as large negative bubbles from extreme market declines. Unfortunately, there has not been a generally accepted definition of what is a financial bubble. Bubbles are more frequent than what you may think as measured by the FCO.

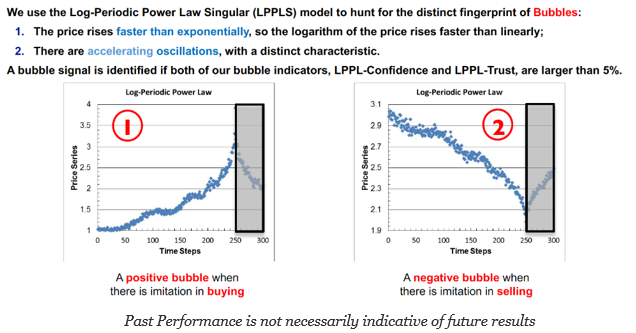

The FCO uses a model that can identify bubbles which also have a high likelihood of bursting through a change in regime. The model looks for price characteristics of a hyperbolic power law and distinct oscillations that usually lead to a price behavior adjustment, reversal, or crash. Simply put, markets that are rising faster than an exponential with greater oscillations are candidates for a bubble. When these characteristics exist, there is a high likelihood of a reversal. What cannot go on for long, will not.

While the fitting of this model is not easy, it provides a framework for comparing large numbers of markets in order to identify bubbles through only looking at price data and not relying on some fundamental valuation or model framework. This is important because an investor can use the output from the FCO through their monthly FCO Cockpit -Global bubble Status Report to identify potential bubbles.

An investor does not have to agree with the FCO on whether the market is showing a bubble, but there is now a well-defined way to identify markets that have bubbles. The FCO identifies markets, sectors, and stocks that fit the LPPLS model and lists them every month. The list can fluctuate from month to month but it is not always short. Bubbles are more frequent than you may think.

Related Posts

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]

The Bankruptcy Cycle Returns: Delayed Failures and the Cost of Easy Money

Proper forest management requires clearing dead brush, protecting high-risk areas, and conducting controlled burns. As January 2026 approaches, marking the one-year anniversary of the devastating Southern California wildfires that destroyed over 16,000 structures, we examine the mistakes made and how those lessons apply to the financial markets. Much like forest fires, risk can be mitigated […]

How Irrational Is It? Valuation Ratios and Bubble Risk

For anyone who has ever ridden a roller coaster, the distinct sound of the chain nearing the top of the first drop echoes in our ears. Click, click, (slower) click…. Anticipation builds right before we experience the massive first drop, picking up speed on the way down. If only the equity markets provided the same […]