Inflation is a growing concern with many investors. Additionally, there is the perception that financial assets are overvalued. There is a need for diversification across other asset classes given the potential for stock-bond correlation rising in an inflationary environment.

It is time to take a closer look at commodities, but there is a little problem. It is not clear how to best access this asset class. One could buy a single commodity manager or a bundle of commodity managers, or one could buy an index-like solution. These index-like solutions could come in three forms, a beta, strategy, or enhanced index. These strategy and enhanced indices may have characteristics like a diversified commodity manager.

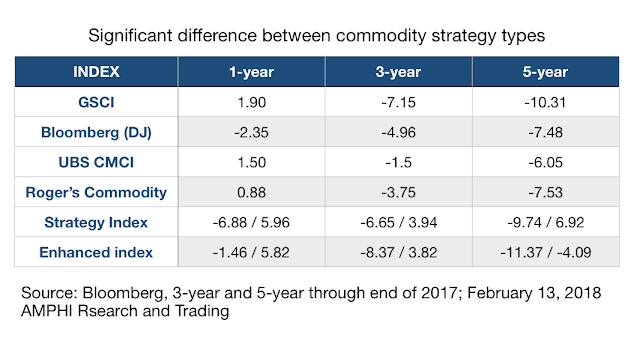

An investor could think that buying a beta index would be easy and would serves as a proxy passive investment in commodities, but the returns across some of the key alternatives would be very fairly disperse. The same would be true for strategy indices which may be driven by factors such as backwardation and contango, or enhanced indices which may include active rules-based long/short decisions. To show the complexity of the index choice problem, we looked at the performance over different time-frames for these three categories as defined by Bloomberg.

Our table presents four popular long-only indices. Each index will have different returns because each has different weighting across commodities, different roll characteristics, and different maturity blends. There is no one standard for beta exposure in commodities. The return dispersion for a long-only index even over the last year would have been four percent. Over a five-year period, the difference would have been 400 bps on an annualized basis. The cumulative effect of choosing the wrong beta index would have had a devastating effect on any commodity portfolio allocation.

The same could be said for strategy and enhanced indices except the impact would be even larger. In the last year, the dispersion in strategy indices would have been over 12.5%. Over a five-year period, the difference would be over 16.50% on an annualized basis. The opportunity to add value relative to a beta long-only index is positive, but the chance of under-performing is real.

Holding your commodity risk in a passive investment whether long-only or some set of risk premiums or factors is risky because the returns across different exposures are highly disperse. Over the last five years, commodity asset class returns were generally negative and choosing an alternative that outperforms the beta exposure is no guarantee of positive returns.

Forward-looking expectations may exceed the past performance for commodities, but the choice of what exposures is complex. Investors will require a strong understanding of commodity dynamics and a willingness to be more active than index investing in stocks or bonds.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]