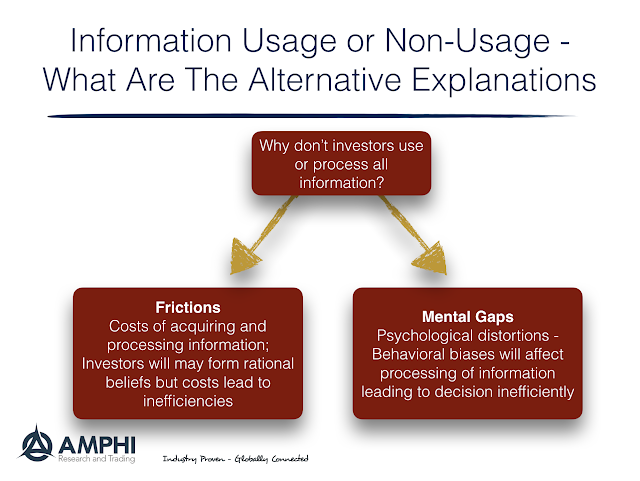

Investors do not always use all the information that is available to them; however this is a not a unique problem to finance but an issue that runs the gamut for all consumer decisions. The explanations for the problem of information usage or non-usage has fallen into two major camps or models of behavior and described nicely in a recent Journal of Economic Perspective article, “Frictions or Mental Gaps: What’s Behind the Information We (Don’t) Use and When Do We Care?” by Benjamin Handel and Joshua Schwartzstein. We present their framework with our view on how the problem can be solved.

One view is that the lack of information usage is associated with market frictions, transaction costs. There is a cost of gathering and processing information so it is not done. This seems unlikely for sophisticated investors, but there is evidence that even simple differences in the costs of index funds are not fully explored by investors. Of course, the cost of processing information may be much higher than the cost of gathering information. If there is a friction, it is with effectively weighting all the information available.

The alternative view is the mental gaps school of thinking which focuses on behavior biases. Investors gather all of the information but they do not use it effectively. It is the poor processing because of mental heuristics which could be the problem with information usage.

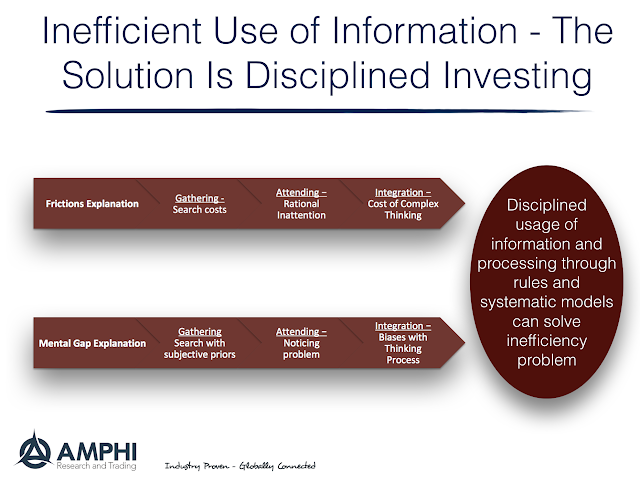

A little of both models can explain decision-making problems in finance. The question is whether there is an effective way to avoid frictions and mental gaps. The problem could be solved through the issue of disciplined systematic decision-making.

For the friction explanation, disciplined investment decisions can use all of the information available and can increase processing through the use of quantitative models. There can be errors with the models, but their effectiveness can be measured and any errors can be adjusted.

For the mental gap explanation, disciplined decision-making can eliminate the problems identified in behavioral finance. Whether anchoring or recency biases, a model or rules-based system can eliminate some obvious behavioral biases.

Markets will always react to surprises in new information, but investors should not be disadvantaged through not using information that is already in the marketplace. Costs can be minimized through effective information gathering and processing which can be done through quantitative tools. Mental gaps can be closed by using rules to hardwire good behavior. There is no reason why information inefficiencies cannot be closed.

Related Posts

Cayler Capital | April Performance Commentary

After finishing off one of the wildest quarters of my trading career, April managed to take the cake. For those that missed it (not sure how you possibly could have), oil settled negative $37. The effects of this were immediate: risk barometers had to be recalculated, option models switched, and most importantly was the immediate […]

Mike Lombardi, football coaching and investing

I am not a football fanatic, but I picked up this book on a recommendation and was amazed by Lombardi’s insights on leadership and management. Mike Lombardi is long-time football executive and media analyst. The book focuses on Bill Belichick and the New England Patriots, but his conclusions could apply to any money management firm. A good money management firm is successful because it acts like a well-disciplined organization with a common purpose. That is no different than a competitively run sports organization. Lombardi finishes his book with five key recommendations for firm success that are worth presenting in bold.

“The Emeril Lagasse Theory” – Practical knowledge and culture is not often transferable

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.