DISCLAIMER:

While investment in managed futures can help enhance returns and reduce risk, it can also do just the opposite and result in further losses in a portfolio. In addition, studies conducted of managed futures as a whole may not be indicative of the performance of any individual CTA. The results of studies conducted in the past may not be indicative of current time periods. Managed futures indices such as the Barclay CTA Index do not represent the entire universe of all CTAs. Individuals cannot invest in the index itself. Actual rates of return may be significantly different and more volatile than those of the index.

Many believe that managed futures are a long volatility strategy because the strategy is like being long a look-back straddle. We believe there is a more nuanced story associated with long gamma exposure, but let’s use the prevailing wisdom of long volatility as a starting point for a discussion.

The question related to the current environment is simple. Should you buy managed futures because volatility is low? Since volatility is low, this could be a good time to buy a “long straddle” strategy. The relationship between low volatility and managed futures can also be viewed through thinking in terms of valuation. Does low volatility mean that managed futures funds are cheap? 2017 inflows suggest that even though recent performance has been negative and many large trend-followers are in drawdowns, investors are putting more money into the space based on an expectation of higher volatility.

So is there evidence of the connection between volatility and managed futures? We have looked at this issue in earlier posts, Managed futures and VIX – beware high daily volatility – embrace high monthly volatility and Managed futures and volatility – The type of vol matters. Our conclusion is that there is no simple answer and there is such a thing as good and bad volatility. Higher long-term volatility which increases the spread of prices is a good for managed futures, but spikes in short-term volatility is detrimental. At tight or range-bound spreads as measured by vol, there may be limited opportunities. If volatility increases and thus increases the range in prices, trend-following should be more profitable. Nevertheless, less, volatility spikes may cause positions to be unnecessarily stopped and thus less profitable.

There has also been some extensive research in this area which suggests that there is a connection between volatility moves and managed futures, but it is also complex and suggests that the trading time frame of the manager matters. This useful analysis was done by Christian Lundstrom and Jarkko Peltomaki in their paper, “Beyond Trends: The Reconcilability of Short-term CTA Strategies with Risk Shocks” in the winter 2015 Journal of Alternative Investments. At a simple level, the researchers found that the VIX level leads to different performance across managed futures styles. They also found that managed futures performance will be impacted by whether volatility changes were expected or unanticipated.

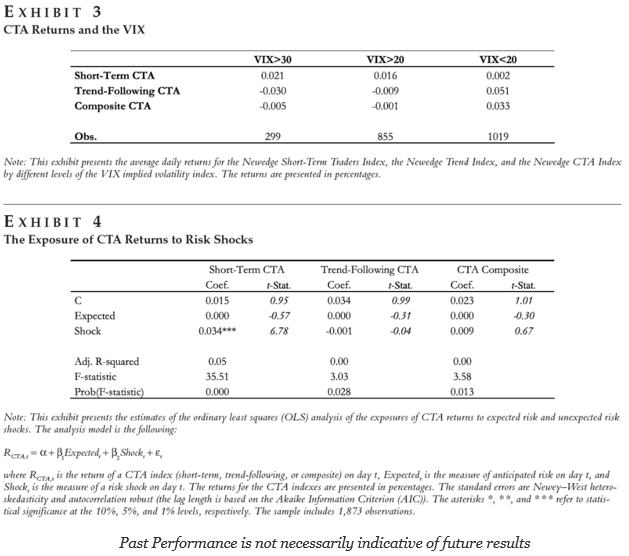

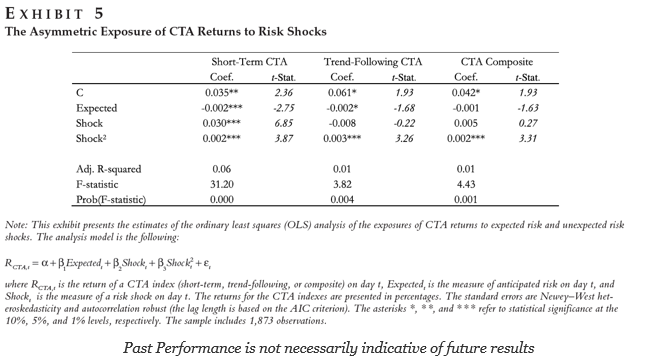

Exhibit 3 shows that managed futures returns are sensitive to the level of VIX. Short-term traders will do better when the volatility is high and trend-followers actually do better when volatility is low. There is a return difference in performance based on the timeframe of the styles used. Exhibit 4 shows that short-term traders do better when there is a volatility shock. Short-term traders will exploit short-term changes in volatility.

A deeper analysis suggests that short-term CTA’s will generate positive returns for volatility shocks and the impact is non-linear. The linear response to shocks is not present for trend-following CTA’s although they also have positive non-linear response to shocks. The return response to expected volatility is slightly negative.

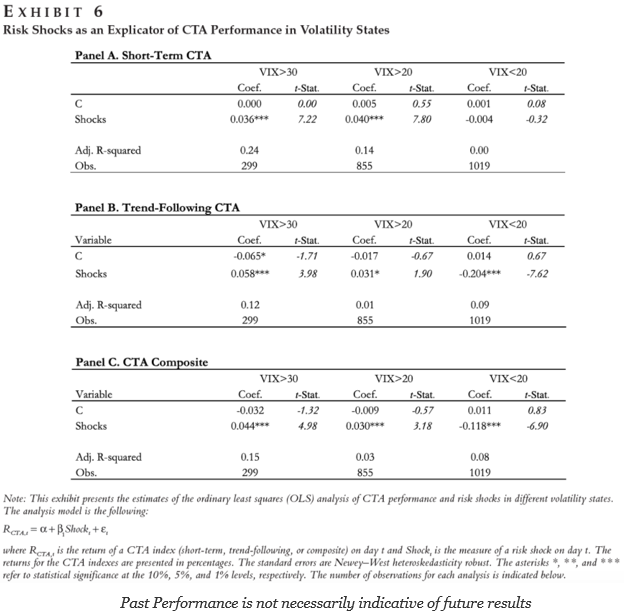

The response to volatility shocks differs with the level of volatility. There will be more positive returns to shocks when overall volatility is higher. There is either an insignificant or a negative response to volatility shocks when volatility is low.

My reaction to this work is that the behavior of CTA’s to expected and unexpected volatility is not completely consistent with descriptions of managed futures strategies and requires more research. The idea that managed futures is a long volatility strategy is not completely validated with respect to the VIX index. Of course, managed futures trade many markets and a single volatility index will not capture the behavior of these other asset sectors. Clearly, the trading time frame has to be matched with the time frame for volatility to get a better representation of style behavior to volatility. Nevertheless, if an investor wants to gain some protection or diversify against equity volatility shocks, he should hold an allocation to short-term CTA managers.