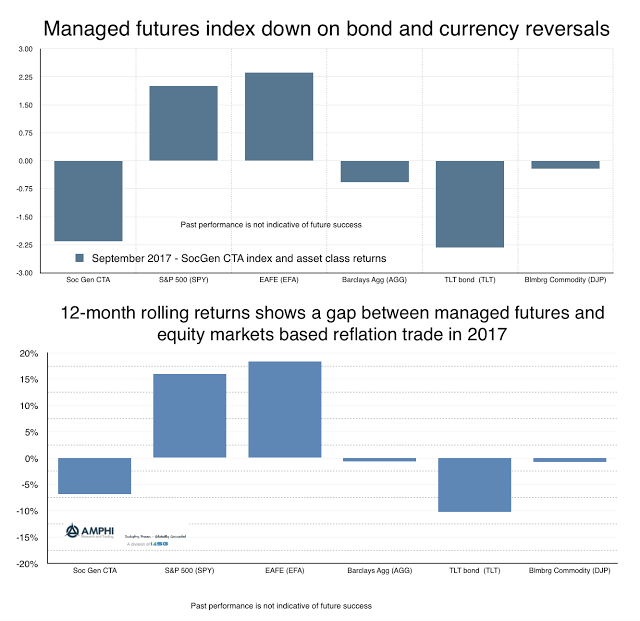

Managed futures returns across CTA’s were down on average for September based on reversals in currency and bond trends. The weakening dollar and the strong bond returns during the summer made for good performance in July and August, but the combination of renewed interest in the Trump reflation trade and uncertainty concerning the direction of interest rates changed the trend opportunities.

Unfortunately, for a trend-based manager, there will be a giveback of some previously accrued profits. Signal identification for exits and new positions is based on price reversals, so changes in directional slope will see negative portfolio returns. Some firms will be better at signal extraction based on the time frame for trades and the any conditional factors, but all will usually see a profit cut. This decline is more pronounced when there are sector changes and not just market adjustments. Given bonds and currency are large sector exposures for many CTA’s, the negative returns should not be surprising.

Managed futures and bonds are strong diversifying assets through their low correlation to equities. A strong equity (risk-on) environment will not be good for “bad times” portfolio diversifiers. There is a cost with diversification.

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]