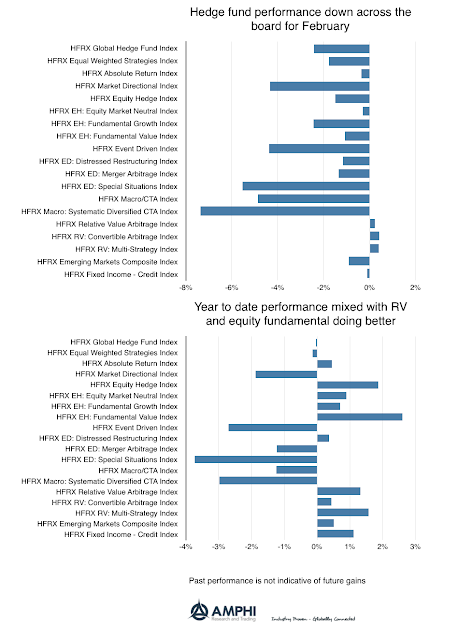

Hedge funds as measured by the HFR indices suffered with the overall market decline with only RV strategies being able to take advantage of the higher volatility environment. In general, the equity hedge fund declines were consistent with their longer-term betas (approximately .3 to .6). The outliers for the month were the event driven, special situations, macro and systematic CTAs indices. The year-to-date returns show significant dispersion with equity hedge fund indices generally positive while special situations, systematic CTAs, and event driven indices falling between -2.50 and -3.75 percent.

There is no way around the fact that hedge fund performance was not pretty. The change in volatility and equity price reversal whipsawed managers, but we are early in the year and the returns are within expected tolerances if we convert annualized volatility into a two-month standard deviation. These periods show greater intra-strategy manager dispersion. There are clear differences in manager skill. This offers an opportunity to reset allocations based on the ability of managers to weather financial shocks.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.