Category: Managed Futures

Active Cash Management for Managed Futures – A Simple Addition to a Fund’s Return Profile

Managed futures have unique features given that margin is only a small potion of the total investment. This allows for active collateral management in ways that are more impactful from other hedge funds. For most hedge funds that use a prime broker and make long/short equity investments, the focus of collateral management is with reducing the cost of borrowing. For futures, the leverage is not through borrowing but through the ability to increase notional funding based on the level of margin to equity. A good portion of funds given to any CTA is not managed efficiently but rather just held in cash.

Why Now Might Be the Best Time to Invest in Managed Futures

Managed futures have been in a significant drawdown with poor Sharpe ratios over the last two years, albeit October has been a good performance month. Many investors have discussed throwing in the towel and getting out of this hedge fund strategy. New investors have focused on other strategies and not wasted time with CTA’s. A […]

Thoughts of Managed Futures Death Were Premature

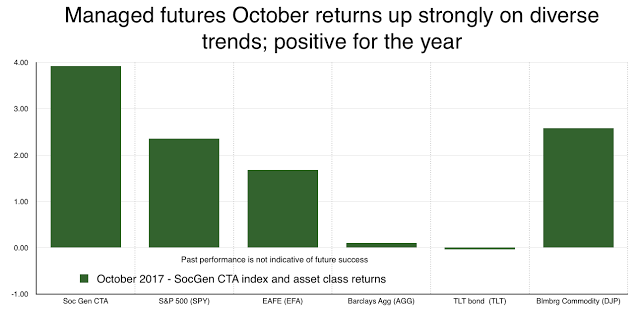

Managed futures returns exploded to the upside with index returns showing big gains relative to alternative asset classes. The positive skew for some managers was even more surprising. We saw some October returns as large as 14%. Every major index we track was close to 3% or higher. For example, the October return using the Morningstar managed futures category was positive 3.45 and the year to date return was up 1.85 percent.

Col. Jessup, Managed Futures, and Code Red for Liquidity

As we approach year-end, it is a good time to think about liquidity and exit strategies from current allocations. Many alternative investments are just not liquid when you need it, even if it is a daily fund. Of course, there is a price or cost with liquidity. Investors may exit but at onerous levels; however, those alternatives that focus trading on liquid instruments will have an advantage over complex strategies or funds that focus on asset that have lower liquidity to start with. Searching for liquidity in a market downturn is a losing game.

Back to Basics on Managed Futures with AIMA – Answering the Question for Why This Strategy Should be Held

There are many works on managed futures that explain the basics of this hedge fund strategy, but the characteristics need to be reinforced especially at current times when the strategy is underperforming other hedge fund strategies. The core reason for holding managed futures is that it provides useful diversification. This diversification is not available from other strategies and this diversification will be especially present during ‘bad times” of a equity decline. Don’t forget that those strategies that have more systematic risk will need to generate higher returns. Investors will be paid to hold them. On the flip-side, there will be a “payment” for managed futures which does well in “bad times”.

Managed Futures Turn Negative on the Renewed Interest in the “Reflation Trade”

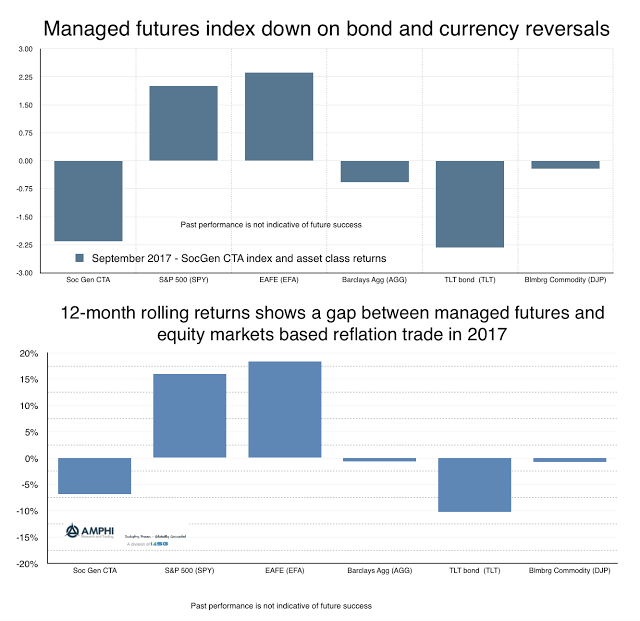

Managed futures returns across CTA’s were down on average for September based on reversals in currency and bond trends. The weakening dollar and the strong bond returns during the summer made for good performance in July and August, but the combination of renewed interest in the Trump reflation trade and uncertainty concerning the direction of interest rates changed the trend opportunities.

Keeping it Simple with Explanations – An Investment Narrative needs to Answer Key Questions

There are two communication problems with global macro investing. First, the stories used to explain the global macro economy are confusing, contradictory, and haven’t proved to be true. This is an outgrowth of the poor forecasting of macroeconomics in general. Second, the stories used to explain the investment process especially for quants goes over the head of most investors. A discussion of techniques is not an explanation for how returns can be generated. Managers need to work on their narratives to ensure that investors understand what they do and why they make money.

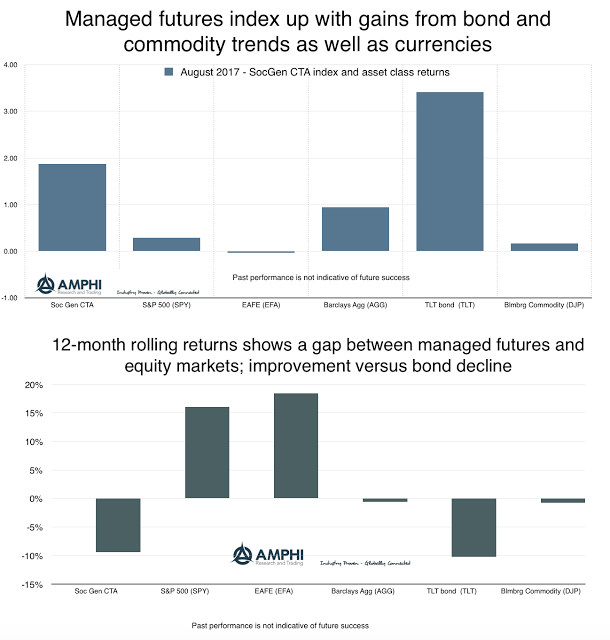

Managed Futures Post Gains on Bond and Currency Trends

Many CTA managers posted gains for August based on strong bond moves in the US and up trends in European fixe income. Currencies continued to add to profitability albeit the decline in the dollar has a flatter slope than previous months. Gold trading was profitable for those who traded it in tandem with currencies. Equity index trading was a more difficult sector given mid-month spikes in volatility and a reversal in direction during the second half of the month. Commodity trading was mixed for many managers with profitability associated with market allocation and style of trading employed. Oil trended lower while refined products and natural gas were slightly up for the month. Hurricane Harvey volatility affected position-taking at the end of the month. Industrial metals have continued their summer upward trends which has caused renewed interest in this sector.

Global Macro – Managed Futures as an Alternative to Corporate Bonds

Corporate bond risk is rising. Of course, with improvement in the overall economy and continued bond flows many will not believe it, but the statistical data suggest that spread moves are no longer symmetrical. There is more potential for spread widening versus continued tightening.

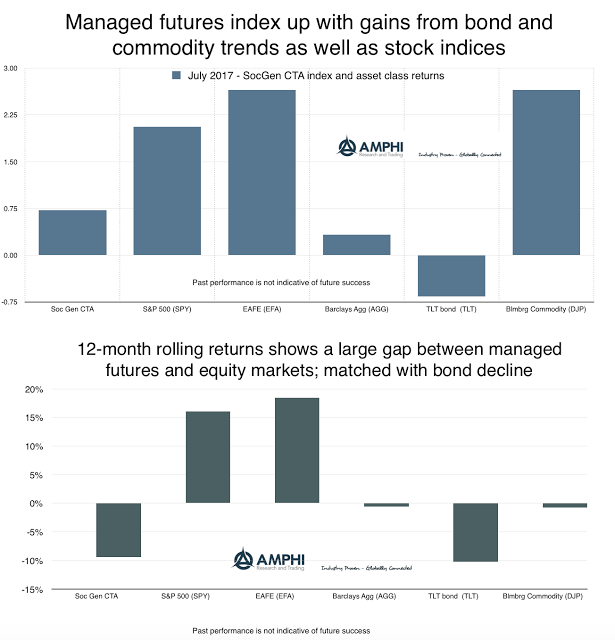

CTA’s Find Trends to Reverse Some of Last Month’s Poor Performance

The month began with some very promising trending opportunities, but with some choppy moves in both bonds and commodities, returns were generated by those who were nimble at position-sizing and getting out of losing trends before profits were completely given back to the market. This was a month where trend timing length mattered. Long-term trends ride through short-term choppiness. Short-term trend following is often able to profit and exit on reversals. A difficult problem is matching model to trend length and is often the reason for a diversity of timing models.

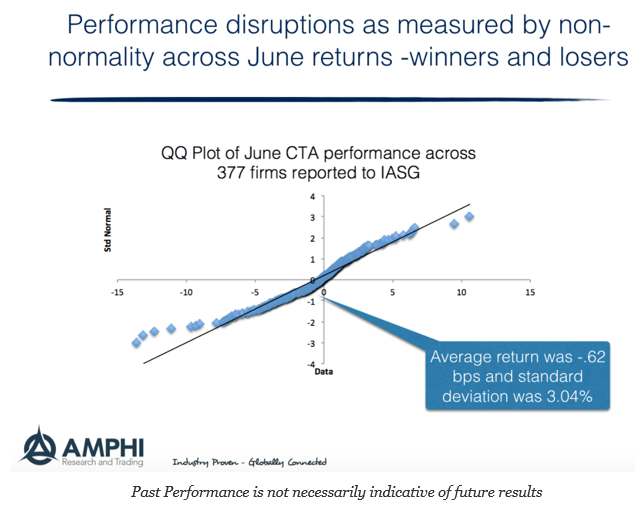

When Markets Disrupt, So Does Performance – June Managed Futures and Outliers

What kind of month was June for CTA’s? Well, you can look at the distribution plot of returns for the month to get an idea of the extremes. We created the QQ plot for the 377 firms that reported to the IASG database for June as of last week. This can be done for smaller more specialized samples, but we took the maximum set of data reported to IASG.

Managed Futures Hit with Trend Reversals, but Opportunity Potential in July

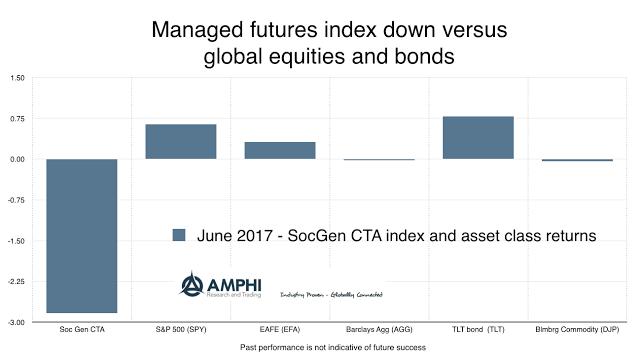

The managed futures index from SocGen was down over 2% for the month with price declines in many major financial markets over the last week. Similar performance has been found with other indices; however, those managers with more commodity diversification have fared better.

Mixing Collateral with a Managed Futures Portfolio – Need to Know Marginal Contributions

In an earlier post we discussed the issue of using capital more efficiently in a managed futures investment. The premise is simple. If only limited funds are used for margin, the majority of cash associated with a managed futures investment are held in low interest investments. This portion of the managed futures capital can be better deployed to increase returns. Similarly, managed futures can be used as an overlay to an existing portfolio to better use cash. See “Use your collateral wisely and enhance managed futures efficiency”.