Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere.

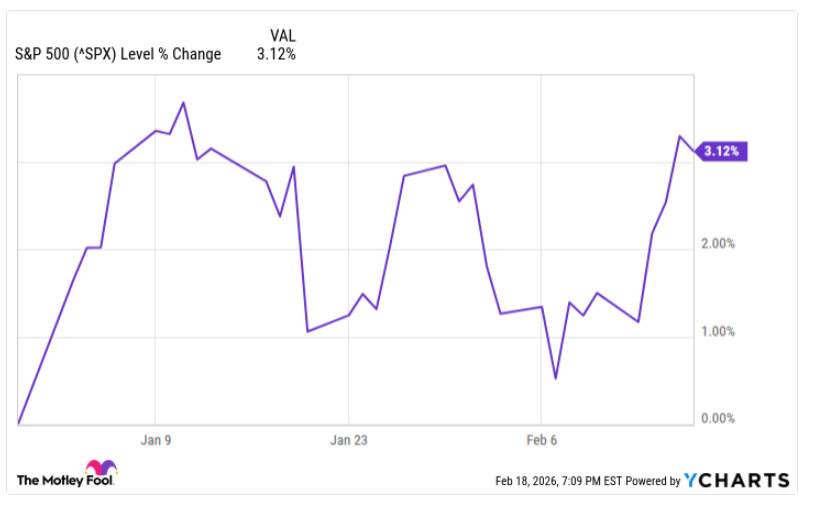

As of mid-February, the S&P 500 is in its narrowest trading range in 50 years. Interestingly, many individual stocks are showing far more volatility than usual. We often see these consolidation periods after large gains or losses, as the market pauses to decide its next direction. Rather than signaling stagnation, they frequently precede a significant move. Below, we examine some leading candidates for big shifts ahead.

Key Takeaways

- The S&P 500 is trading in its narrowest range in nearly 50 years.

- Leadership from the Magnificent Seven may be fading.

- Metals markets remain volatile due to geopolitical tensions and demand from the energy transition.

- The U.S. dollar’s recent weakness could influence commodities and global markets.

- Consolidation periods often precede large market moves.

The “Magnificent Seven” and Equity Leadership

Warren Buffett is famous for his performance against the S&P, the benchmark by which most funds judge themselves. After a hot start, it has gone almost nowhere. History offers context. In 2005, the index gained only about 3% for the full year. Yet 2006 delivered a solid 14% return following a similar quiet period.

This year, the performance of the so-called “Magnificent Seven,” which includes titans like Google, Apple, Nvidia, Microsoft, and Tesla, is down in many cases. This marks a big shift from the preceding period, when these names pushed indices higher almost by themselves. According to economist Larry Swedroe, these stocks drove 40% of the total index returns for 2025. Their valuations bring warning signals as their collective P/E ratios averaged 64, which is reminiscent of the Dot.com bubble and previous periods of exuberance. We discussed many of these ratios in November.

Swedroe warns that retail investors often buy these names near peaks and sell near troughs. He suggests that sectors with more historically normal valuations—such as healthcare, energy, and defensive consumer staples—could take over market leadership. Trillions in planned data-center spending may also boost demand for materials, power infrastructure, and utilities. With former leaders faltering, a rotation into more defensive areas feels plausible, especially if tariffs or geopolitical tensions accelerate the move.

Metals Market

We discussed the explosive upward movement in metals as January ended on a spectacular note. Silver saw a dramatic 34% intraday plunge late in January before stabilizing in a tighter range during its recovery. Gold followed a similar trajectory but rebounded more convincingly. Copper, by contrast, has struggled to break higher, weighed down by fears of slowing global growth.

The earlier surge across metals stemmed from two main drivers: their traditional role as safe-haven assets and rising structural demand tied to energy transition (batteries, renewables, grid upgrades). While Bitcoin briefly challenged gold’s status as an alternative “currency,” it has since fallen roughly 50% from its all-time high—whereas gold and silver remain near record levels.

People often view metals as an alternative to currency, so it makes sense to look at these in the context of various denominations. Fed policy and tariff uncertainty provide additional confusion on what the next direction might be for both sectors. More on those next.

Metals Snapshot (Feb 2006)

| Metal | Recent Price/Range | Key Drivers | Consolidation? |

|---|---|---|---|

| Gold | ~$5,000-$5,200/oz (peaks >$5,100) | Geopolitics, tariffs, central banks, dollar weakness | Yes, high-range with volatility |

| Silver | ~$80-$91/oz (peaks >$100) | Safe-haven + industrial deficits, tariffs | Partial; elevated ranges, some flags/sideways |

| Copper | $5.90-$6.00/lb ($13k/t) | AI infrastructure, electrification demand, supply issues, tariffs | Yes, clear zones |

| Aluminum / Nickel / Zinc | Mixed, aluminum elevated but pressured | Supply caps, regional premiums, China demand | Range-bound and choppy |

Currencies

The US dollar declined markedly in January, alongside metals, reaching a four-year low after comments from President Trump downplayed concerns about its strength. His push for a more dovish Federal Reserve and further rate cuts encouraged investors to move out of the currency. This weaker dollar appears intentional: it boosts the competitiveness of US exports while making imports more expensive.

Even so, US interest rates (around 3.75%) remain among the highest globally, comparable to those in the United Kingdom and Australia. The Australian dollar (AUD) benefited from the initial rotation away from the USD before stabilizing in its own range. Meanwhile, Mexico continues to stand out with a policy rate near 7%, drawing strong capital inflows. Ongoing cartel-related violence remains a key risk to this stability.

Overall Market Outlook

Markets often pause to catch their breath before the next major leg. These inflection points also carry the risk of a sharp break, up or down.

The good news? Valuations in many sectors remain reasonable, and the most extreme FOMO-driven trades appear to be cooling. With ongoing uncertainty out of Washington and mounting geopolitical pressures (including potential regime change in Iran), conditions can shift rapidly.

For now, enjoy the relative calm—and make sure your portfolio is positioned for whatever comes next.

FAQ

Why is the S&P 500 trading in such a narrow range?

Consolidation often follows strong gains or losses, when investors pause to reassess valuations and policy expectations. These periods can look quiet at the index level even while single stocks remain volatile.

What are the “Magnificent Seven” and why do they matter?

The Magnificent Seven refers to the largest mega-cap tech stocks that have driven an outsized share of index returns. If they stall, leadership can rotate to sectors with more normal valuations.

Why are metals volatile right now?

Metals are being pulled by competing forces: safe-haven demand, electrification-driven structural demand, and uncertainty around tariffs, growth, and central bank policy.

How does the U.S. dollar affect metals?

Because metals are priced in dollars, a weaker USD can support higher metal prices globally. If the dollar stabilizes or strengthens, it can become a headwind—especially for the more cyclical metals.

Sources & References

- Historical market consolidation analysis:

https://www.fool.com/investing/2026/02/22/the-sp-500-is-stuck-what-history-says-happens-next/ - Larry Swedroe’s commentary on market behavior:

https://larryswedroe.substack.com/p/ten-lessons-the-market-taught-us - Market chart data and price visualization:

https://www.tradingview.com/ - Global interest rate comparisons:

https://tradingeconomics.com/country-list/interest-rate

Illustration created by ChatGPT (OpenAI / DALL·E)

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]