I would not be the first to engage in the lazy thinking that managed futures are synonymous with trend-following. There was little wrong with using both terms to mean the same thing for many years. The majority of managed futures are still trend-following.

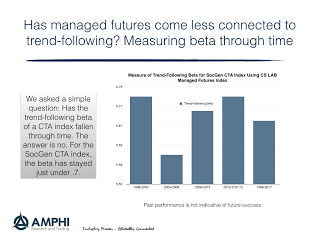

We ran a non-overlapping regression using five years of monthly data to measure the trend-following beta of the SocGen CTA index, a peer group index of managers. We used the CS Liquid Beta managed futures trend-following index as the proxy for trend-following. The numbers suggest that the beta is about the same for a widely followed peer index since 1998 at approximately .7.

However, the last year or two suggests a growing gap within the managed futures strategy space that will not be picked up within the trend-following beta of a peer group of primarily large managers.

The business strategy gap has been the growing marketing push to sell trend-following as a low-cost quant strategy. We are now seeing some leading firms market their trend-following strategy at flat fees of 50 bps. The same firms may have other futures-based strategies at higher fees, but actually market a “pure” or “stripped-down” version of trend-following as a low cost product.

This product pricing push has changed the revenue model for these firms. There may be more money coming into managed futures, but it is at lower fees; consequently, there has been a move to develop new strategies explicitly marketed as non-trend-following quant or trend-following plus.

These products have added models attached to a core strategy. Complexity has been added to either justify higher fees or differentiate product offering from the core trend product. Hence, it is becoming harder to analyze managers in this strategy space. Investors will have to implement some form of core-satellite between trend and non-trend managers to access the best managed futures alternatives.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]