One way to measure market uncertainty is to run a simple thought experiment. A well-behaved market should match performance with events in a well-defined manner. An uncertain, complex market environment would behave in an ill-defined manner. Close your eyes and assume you know the news highlights for May. For example:

- Political turmoil in Italy and the EU

- Off-again/on-again North Korea talks

- Good economic data albeit with lower momentum

- EM problems in Turkey and Argentina

- Trade war discussions

What would you expect?

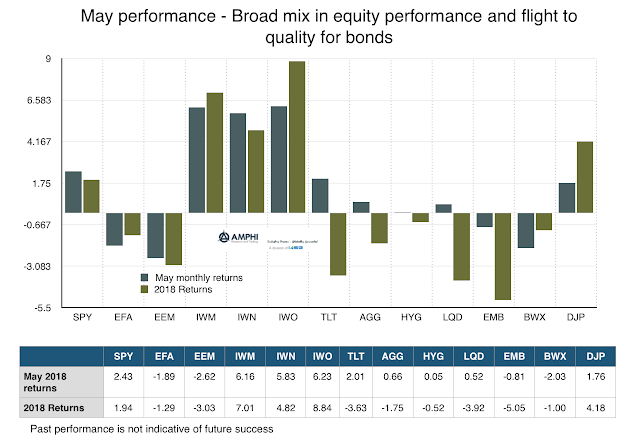

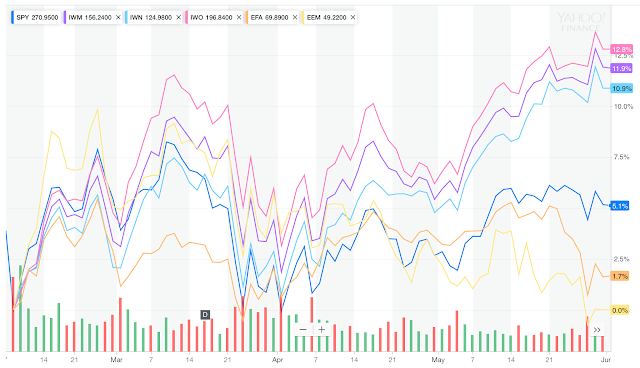

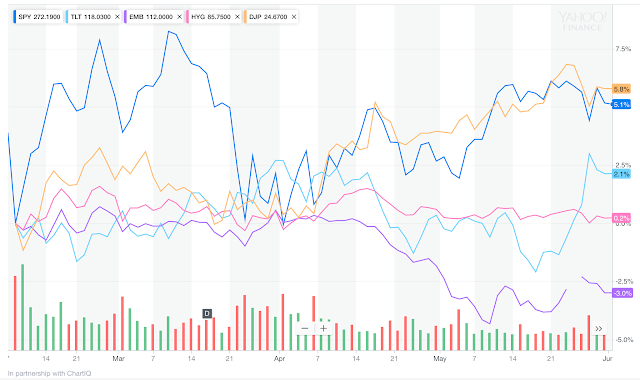

The results for May were quite different from what many would expect for some asset classes. A flight to quality and a Treasury rally seems consistent with the news. Similarly, a decline in developed equity and emerging markets also seem consistent. However, the strong showing with small-cap, value, and growth are out of character in the current environment.

Small cap, growth, and value indices all had gains of over 5 percent for the month, even with higher volatility in the last week. Core domestic equities did better than global, emerging, and large-cap stocks. These numbers are inconsistent with a flight to quality or risk-off behavior by some international investors. Unfortunately, the critical drivers for May are political headline risks which are difficult to handicap. There is little evidence that can be used to provide a likelihood for further momentum or mean reversion.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]