There should be concerns about the amount of corporate leverage in the economy, but if there is no catalyst credit event, current risk is limited. We are not downplaying potential credit risk, but there needs to be focus on the right issues that will drive corporate bonds spreads higher.

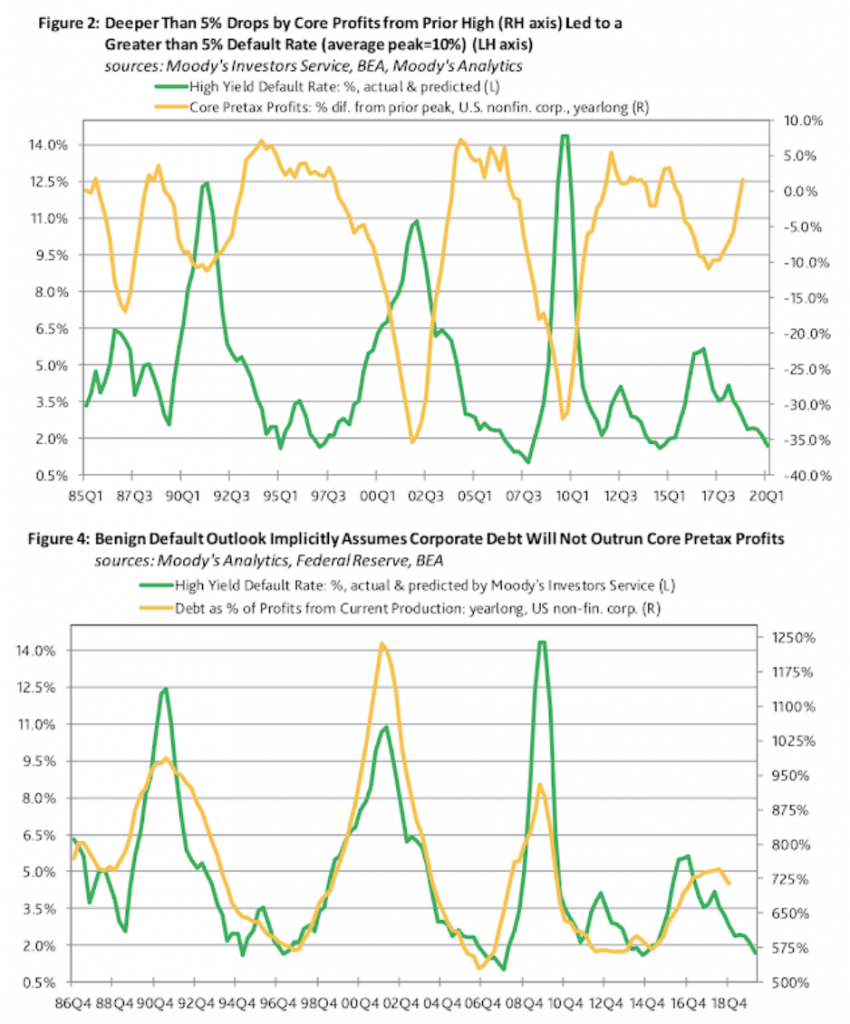

If corporate profits fall, there will be an increase in the high yield default rate. Follow the profits, and with profits moving higher, default rates have fallen. See Moody’s Analytics, “Benign Default Outlook Implies Profits Will Outrun Corporate Debt”. If the profit environment changes, credit risks will respond.

Debt as a percentage of profits is more important than debt as a percentage of GDP. The size of the debt to GDP may not forecast defaults but it does tell us the potential for severity if there is a profit decline. Consequently, following forward guidance on earnings may give an early signal on potential default and widening of spreads. Currently, earnings guidance has turned negative, yet we are seeing that earnings have been more robust than forecast last quarter. For the first quarter, approximately 2/3rds of companies reported earnings or a revenue surprise. Nevertheless, earnings guidance has turned negative for the first time in two years. This suggests that we may be on the cusp for changes in spreads.

Related Posts

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]

The Bankruptcy Cycle Returns: Delayed Failures and the Cost of Easy Money

Proper forest management requires clearing dead brush, protecting high-risk areas, and conducting controlled burns. As January 2026 approaches, marking the one-year anniversary of the devastating Southern California wildfires that destroyed over 16,000 structures, we examine the mistakes made and how those lessons apply to the financial markets. Much like forest fires, risk can be mitigated […]

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]